Women

Partner Channels: Auctions | Auto | Bill Pay | Jobs | Lifestyle | TechJobs | Technology | Travel

April 17, 2001

|

|

|

|

|

|

||

|

Channels: Astrology | Broadband | Chat | Contests | E-cards | Money | Movies | Romance | Search | Weather | Wedding Women Partner Channels: Auctions | Auto | Bill Pay | Jobs | Lifestyle | TechJobs | Technology | Travel |

||

|

|

||

|

Home >

Money > Mutual funds > Fund File April 17, 2001 |

Feedback | |

|

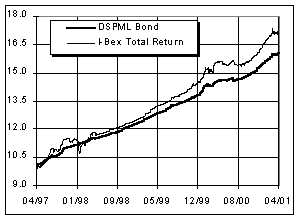

DSPML Bond FundDhirendra Kumar DSPML Bond Fund, a medium-term debt fund was launched in April 1997. The fund seeks to generate an attractive return consistently with prudent risk management. In its dividend plan, it has paid dividends aggregating to 12 per cent in 1998, 13.7 per cent in 1999, 9.6 per cent in 2000 and 5 per cent so far in 2001. Investors can enter and exit at NAV.

The focus on AAA rated instruments is consistent with its strategy of limiting risk, for these instruments are high on credit quality. Further, they offer a great degree of flexibility in handling large-scale redemption. However, the high quality focus limits the coupon interest earned by these instruments though the fund has sought to mitigate the same with interest rate management. Bonds lose value when interest rates go up, with longer dated portfolio being more sensitive to interest rate changes. While a triple A portfolio with its liquidity, is more susceptible to volatility, it can be handled by changing the portfolio maturity. With the interest rate cut in early 2000, the fund aggressively stretched its maturity to 6.82 years in early 2000. However, with sentiments turning weak subsequently, it dexterously realigned to lower maturity spectrum. In the two years ended March 31, the fund has returned 12.65 per cent against a category average of 12.40 per cent.

With an ideal size of Rs 8.70 billion, DSPML Bond is well positioned to pursue a nimble-footed strategy. Further, it has handled the pressure of institutional investments by holding a liquid portfolio. With an active and quality conscious management, the fund has posted a reasonable return of 12.58 per cent in its four-year tenure, consistent with the philosophy of safety of capital over returns.

Source: Value Research

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

With a focus on credit quality, the fund has structured its medium sized corpus around a quality portfolio. The focus on portfolio quality has been retained since inception, with AAA rated instruments averaging at 88 per cent in the last trailing year. While the fund parked in corporate instruments earlier with a growing corpus, it was one of the first schemes to invest in government securities. While the fund has had exposure to lower rated papers, the same has been capped at around 10 per cent of the corpus.

With a focus on credit quality, the fund has structured its medium sized corpus around a quality portfolio. The focus on portfolio quality has been retained since inception, with AAA rated instruments averaging at 88 per cent in the last trailing year. While the fund parked in corporate instruments earlier with a growing corpus, it was one of the first schemes to invest in government securities. While the fund has had exposure to lower rated papers, the same has been capped at around 10 per cent of the corpus.